What's the difference between EMI, growth shares, and unapproved options?

Compared to other share option schemes available to UK-based businesses, EMIs are the most tax-efficient option for both businesses and employees.

Tax is incurred only on the value of the shares at the time of their award rather than at the time of exercise (at which their value may have risen).

Additionally, Capital Gains Tax (CGT) is applied at a lower rate versus the standard rate (so long as the shares are not sold within 24 months of the option grant).

That's because EMI options are eligible for Business Asset Disposal Relief (BADR) so long as a few conditions are met. At present, the rate is 14% and will remain that way for the rest of the current tax year. In the 2026/27 tax year, it will rise to 18%.

Standard Capital Gains Tax is now charged at 18% for basic rate taxpayers, or 24% for higher or additional rate taxpayers.

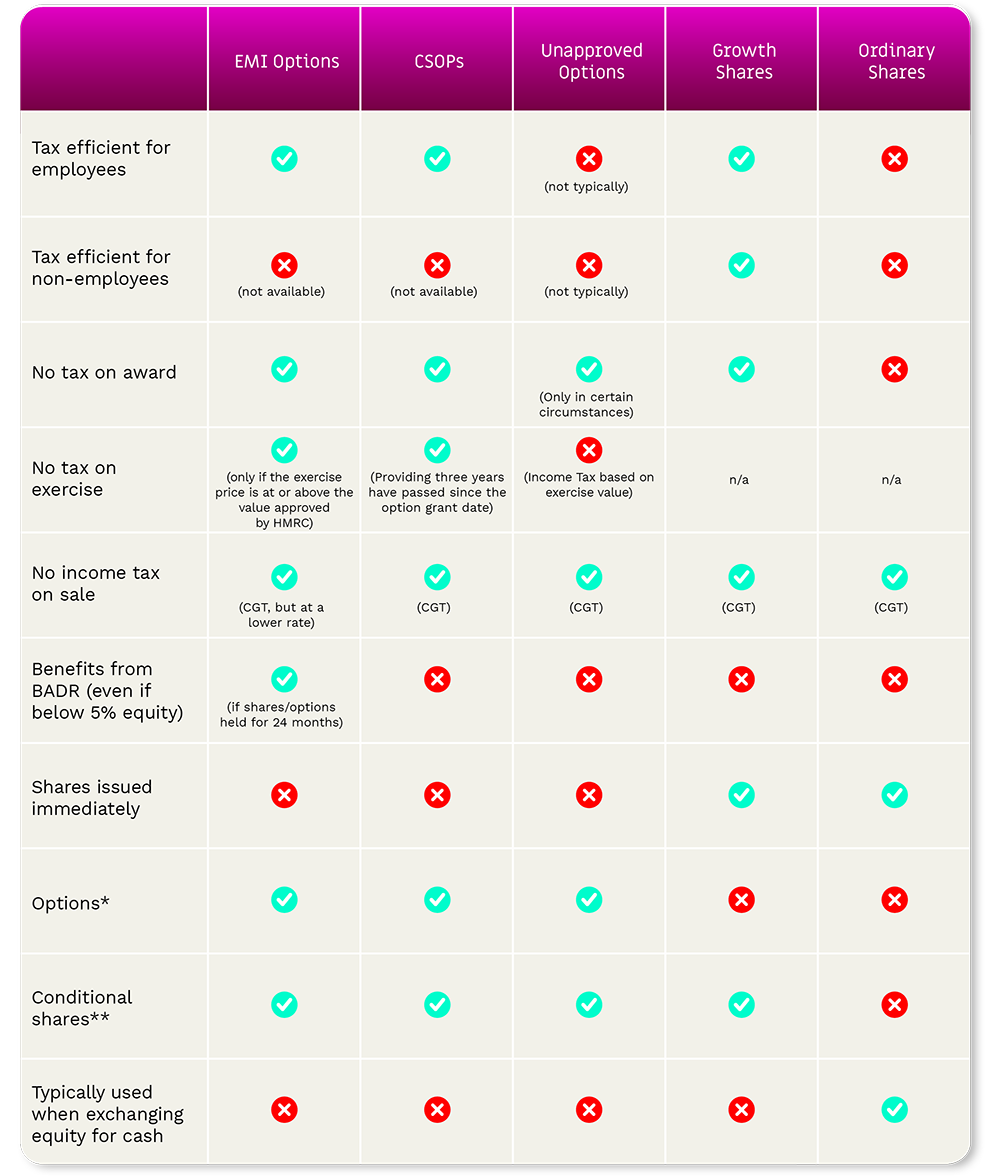

The chart below outlines the main differences between EMI options, CSOP options, growth shares, unapproved options and ordinary shares. (Click to enlarge).

Due to its requirements and tax advantages, an EMI share scheme is most attractive to UK-based SMEs seeking to share their success with a small to medium-sized team (under 250 employees).

What are the tax implications of Enterprise Management Incentives for my company?

Businesses offering EMIs are eligible for a corporation tax (CT) relief if qualifying shares are acquired by employees upon the exercise of an EMI option.

The CT relief is typically the difference between what the employee pays for their shares and their value when their options are exercised.

What about my team?

Employees receiving option grants via an EMI scheme are eligible for Business Asset Disposal Relief (BADR), formerly known as Entrepreneurs' Relief, at the time of sale.

This tax relief allows for a discounted rate (versus the standard rate) on any gains on the actual market value (AMV) of shares at the time of grant, so long as the shares are sold at least 24 months from the date of the option grant.

Disqualifying events

If there is a disqualifying event that causes your business, an employee, or the options scheme to no longer meet the qualifying criteria, the options will lose their advantaged tax status unless they are exercised within 90 days of the event.

For more details on the tax implications of EMIs, we suggest reading one of the pages linked above, this summary or seeking advice from your tax professional.

What happens to an employee's EMI options if they leave?

An employee leaving the company is classed as a disqualifying event. So employees must exercise their EMI options within 90 days, otherwise, any gains will be subject to Income Tax and possibly National Insurance.

Watertight EMI option agreements include leaver clauses, which outline what will happen to an employee's options depending on the circumstances surrounding their departure.

If an employee has truly earned their slice of the pie, we see no reason why they shouldn't get to share in the value they helped to create. That's where the notion of 'good leavers' and 'bad leavers' comes in.

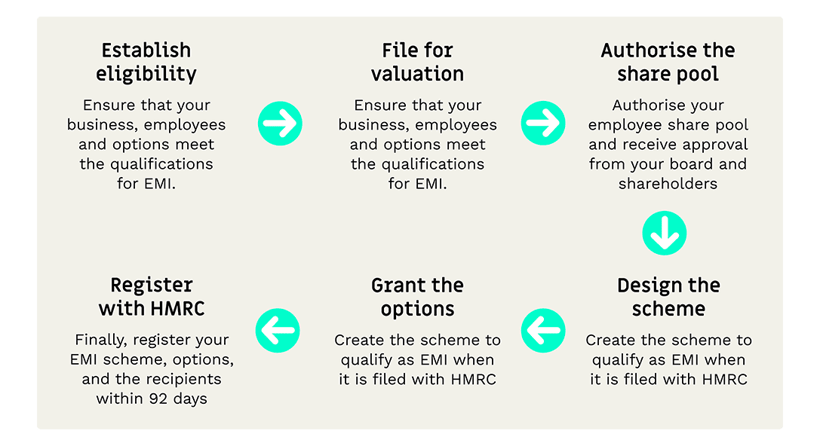

What does the EMI scheme setup process look like?

Once you have established your eligibility for Enterprise Management Incentives, the owner must file with HMRC to receive a valuation for approval. It's valid for 90 days and provides some certainty regarding tax treatment going forward, as long as all due criteria and processes are followed.

Once the valuation is agreed upon, you will need to authorise your employee share pool and receive approval from your board and any shareholders. After this, you can design your scheme and grant options to employees.

Finally, your business must register its EMI scheme, options, and recipients with HMRC within 92 days of its first option grant.

This process can be challenging for business owners, who have many other things to focus on. And this is precisely why we built Vestd.

The platform - and our team of EMI experts - can assist with the setup of your EMI scheme, help you generate a valuation and file it with HMRC, create dynamic vesting schedules, and make the long-term management of your issued options easier.

By using our share scheme platform, you'll avoid hassles and unnecessary costs and ensure that your business stays compliant through to exit.

How do I manage an EMI option scheme?

Long term, you will need to manage your Enterprise Management Incentive scheme by adding new recipients, removing recipients, and updating your cap table to reflect the current options issued.

You will also need to notify HMRC of any changes, such as new option grants, employee departures, or a company exit (buyout or change in ownership).

Managing your EMI scheme on your own can be very difficult and time-consuming. And the cost of getting it wrong is dear.

By using Vestd, you will have access to features that help you manage your scheme without any hassle.