Simon Telling

Simon Telling

EMI, Unapproved Options & Growth Shares: What's right for you?

Last updated: 6 February 2024. EMI options, unapproved share options and growth shares all have their benefits, but one may be a better fit for your...

Manage your equity and shareholders

Share schemes & options

Equity management

Migrate to Vestd

Company valuations

Fundraising

Launch funds, evalute deals & invest

Special Purpose Vehicles (SPV)

Powerful tools and five-star support

Employee share schemes

Predictable pricing and no hidden charges

For startups

For scaleups & SMEs

For larger companies

Ideas, insight and tools to help you grow

Updated 06 February 2024.

We spend a lot of time talking to business owners about different types of shares. Quite often it’s not as simple as ‘this type of share scheme is the “best” for your business’ because many different factors come into play.

So we’ve created the unapproved options vs growth shares calculator to help you figure out the difference in net benefit, as that’s a good place to start.

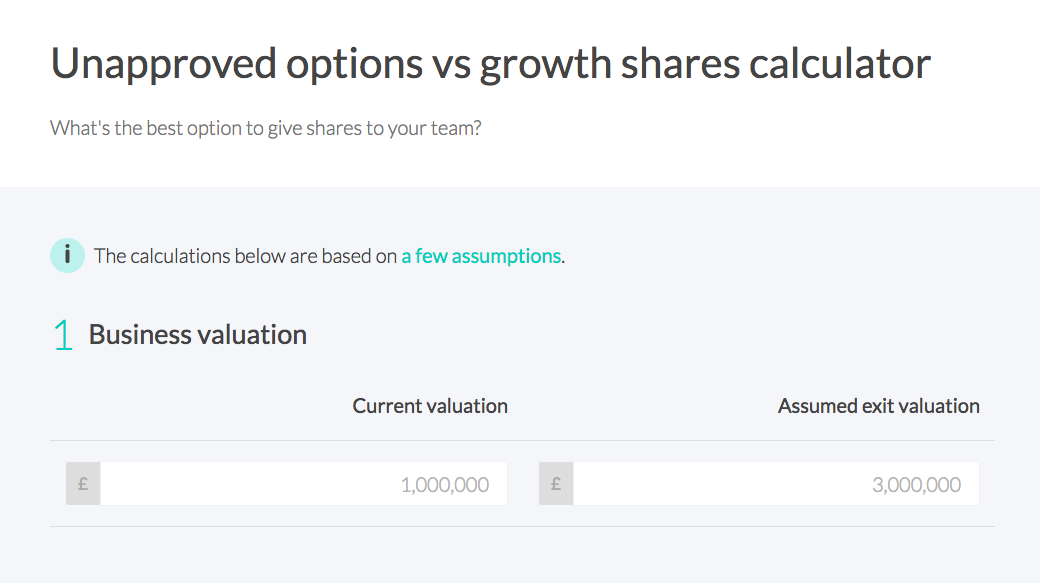

You start with an estimate of the business value today and assume a future exit valuation (you are allowed to dream at this stage, but more helpful to be objective).

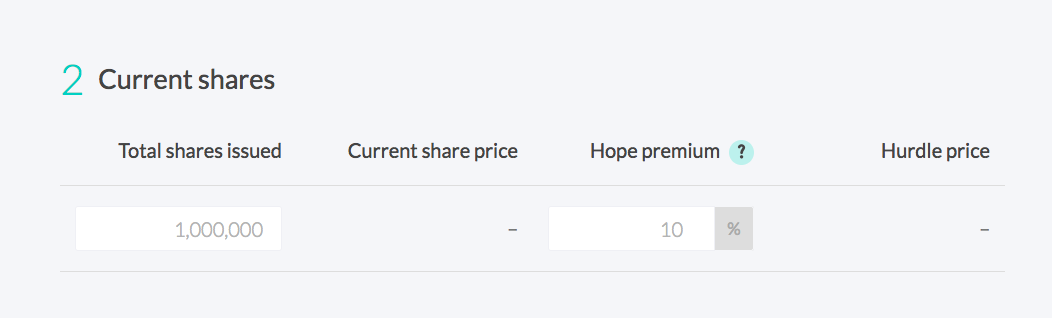

Enter the total number of shares you’ve issued, and your hope premium. The ‘hope premium’ is the marginal uplift on your valuation of shares at the time of issue (AKA the 'hurdle').

This is to make sure HMRC are comfortable that no tangible value has been transferred without being taxed (typically 5–20%). The calculator will then quickly work out your current share price and what the hurdle price would be for growth shares.

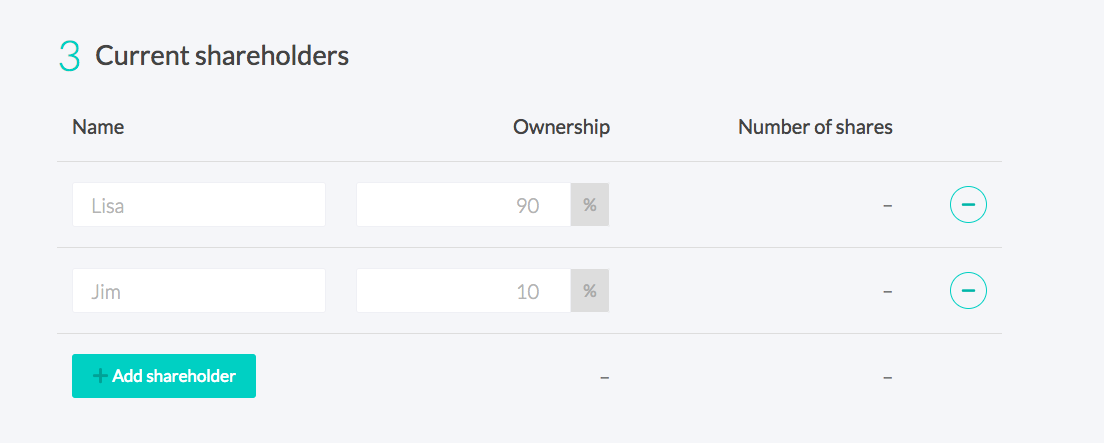

Just pop in their name and percentage of ownership. The calculator will tell you what that means in terms of number of shares.

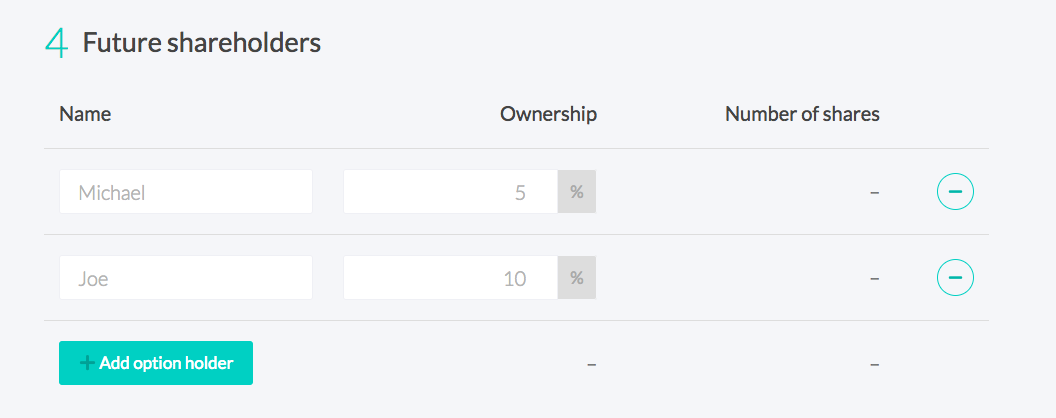

Same details as existing shareholders but for your lucky new ones.

This is the magic bit. From the information you’ve added the calculator has worked out the net benefit for each recipient for both unapproved options and for growth shares. So you can easily see which one works out best for your shareholders.

If you’re ready, go ahead and get started comparing growth shares and unapproved options. But if you want a bit more information first, keep on reading.

Unapproved options are pretty simple. They are also flexible and can be given to employees, contractors, advisors, consultants, you get the picture.

Another factor adding to the simplicity is that unapproved options don’t require any formal valuation or notification to HMRC when the options are set up (unlike EMI), although they do need to be included in an annual report to HMRC via ERS if they have been given to employees or directors.

The big disadvantage with unapproved options is that there is no tax benefit for the recipient. The recipient is liable for income tax on the difference between the exercise price and the market value of the shares at the time.

An employee may also be liable to pay national insurance on this, if the shares are readily convertible to cash at the point of exercise (eg in a sale scenario).

Growth shares only share in the capital growth of the business from the point that they are issued.

For example, if they are issued at a hurdle of £1 per share, they will only share in any eventual net sale proceeds that are over and above £1 per share. This means that existing shareholders are only value diluted for growth from that point, rather than the existing worth of the company.

So, recipients of growth shares don’t have to pay income tax on exercise, only capital gains tax on sale (which is the same for unapproved options). This makes them pretty tax efficient for non-employees and, if you’ve previously used EMI options for employees, tax efficient for them too.

They can be issued immediately and (again, the same for unapproved options) it’s possible to set conditionality for the shares.

Well, unapproved options are simpler, you don’t need to adopt new articles of association and they are much more commonly understood. And, if the business has limited growth potential, say less than two or three times current, then unapproved may actually be more efficient.

Don’t miss out on setting up the perfect share scheme for your team - start right by using the calculator. Then, talk to an equity specialist to get your growth share scheme or unapproved options scheme underway.

Last updated: 6 February 2024. EMI options, unapproved share options and growth shares all have their benefits, but one may be a better fit for your...

If you’re looking to incentivise or reward someone with a stake in your business, who isn’t on the payroll or doesn’t qualify for EMI options,...

Last updated: 23 November 2023. There are many different ways to share ownership. EMI options are the most tax-efficient for your employees. Growth...