Sapta

Sapta

Fair Market Value (FMV) explained for startups

Imagine you're one of the first employees at a fast-growing startup. Along with your salary, you're offered 20,000 ESOPs. It sounds exciting, but...

Employee share options have created millionaires, rewarded early believers, and helped some of the world's fastest-growing companies attract exceptional talent. But there's one catch: receiving options doesn't mean you own them yet. That's where vesting comes in.

Vesting determines when employees actually earn the economic rights to their options. It's one of the most important parts of any employee share scheme, yet it's often misunderstood.

Questions like "When do my options become mine?", "What happens if I leave?", and "Will I keep my equity if the company is acquired?" can significantly affect the value of an equity package.

In this blog, we'll answer the most common questions about ESOP vesting, using real-world scenarios to bring the mechanics of employee ownership to life. By the end, you'll understand not just what vesting is, but why it can have a bigger impact on your equity than the size of your grant itself.

ESOP vesting is the process through which employees gradually earn the right to exercise their share options over time. When an employee receives an option grant, they don't automatically become a shareholder. Instead, the company sets a vesting schedule that determines when those options become available to exercise.

Shares = actual ownership in the company.

Share options = the right to buy shares in the future, usually after vesting conditions are met.

Think of it as earning ownership over time rather than receiving it all at once.

Many ESOPs include a cliff period, which is a minimum period of employment that must be completed before any options vest. This period is known as the cliff. Under Indian ESOP regulations, options cannot vest earlier than one year from the date of grant, making a one-year cliff a standard feature of most ESOP plans. If an employee leaves before the cliff date, they typically forfeit all of their options. Once the cliff is reached, a larger portion of options may vest at once, after which vesting often continues gradually.

For example, imagine an employee receives 4,800 share options when they join a startup. The company uses a four-year vesting schedule with a 12-month cliff. Rather than gaining access to all 4,800 options immediately, the employee earns them gradually. After one year, they may have access to 1,200 options. After two years, 2,400 options. After four years, the full 4,800 options will have vested.

This approach helps align employee rewards with long-term contribution to the business while giving employees a clear path towards ownership

It's important to note that vesting and exercising are not the same thing. Even after options have vested, an employee's ability to exercise them will depend on the terms of the option agreement and the circumstances of the company.

Many employees confuse these dates and concepts, but understanding the distinction is critical when evaluating the value and practical benefits of an equity package.

A vesting schedule determines how many options vest on each vesting date throughout the vesting period.

Companies can structure vesting schedules in different ways depending on their objectives.

The most common approach.

Options vest in equal portions over a defined period. For example:

A larger proportion of options vest in later years.

For example:

This structure can provide stronger incentives for long-term retention.

All options vest at a single point in time rather than in stages.

For example:

Vesting conditions determine what requirements must be met before options can vest.

The employee must remain employed or continue providing services to the company for the required period.

This is the most common vesting condition used in employee share schemes.

In addition to continued employment, specific performance or business objectives must be achieved.

Examples include:

Pro tip: Performance targets can be tricky unless they’re very specific, measurable and, most importantly, achievable. Time-based vesting is the gold standard; there's no room for ambiguity.

A combination of time-based and milestone-based requirements.

These arrangements are often used for senior hires, founders, or executives where both retention and performance are important.

If companies want employees to benefit from ownership, why not simply give them all their share options on day one?

Equity is designed to reward long-term contribution, not just joining the business.

Consider two employees who receive the same option grant:

This is the challenge vesting was designed to solve.

A vesting schedule ensures that ownership is earned, not simply granted. Rather than giving both employees the same equity outcome, vesting rewards those who stay, contribute, and help create long-term value.

It also protects founders, investors, and existing shareholders by reducing the risk of significant equity leaving the business with employees who depart early. In short, vesting helps align ownership with contribution, making employee equity fairer for everyone involved.

Imagine an employee receives 4,800 share options when they join the company.

The vesting schedule is:

During the first year, none of the options vest. As mentioned above, this period is known as the cliff. Under Indian ESOP regulations, options cannot vest earlier than one year from the date of grant, making a one-year cliff a standard feature of most ESOP plans.

Once the employee reaches their first anniversary, 25% of the grant vests at once. In this example, that means 1,200 options become available.

The remaining 3,600 options then vest gradually over the next three years, typically on a monthly basis. This means approximately 100 options vest each month until the employee has earned the full grant.

The timeline looks like this:

Note: “This example is for illustrative purposes only. Vesting schedules, option grants, and plan rules vary between companies and should not be considered standard terms.”

This approach has become the industry standard because it balances employee ownership with long-term retention. Employees gain a meaningful stake in the company's success, while the business ensures that equity is earned through ongoing contribution rather than awarded upfront.

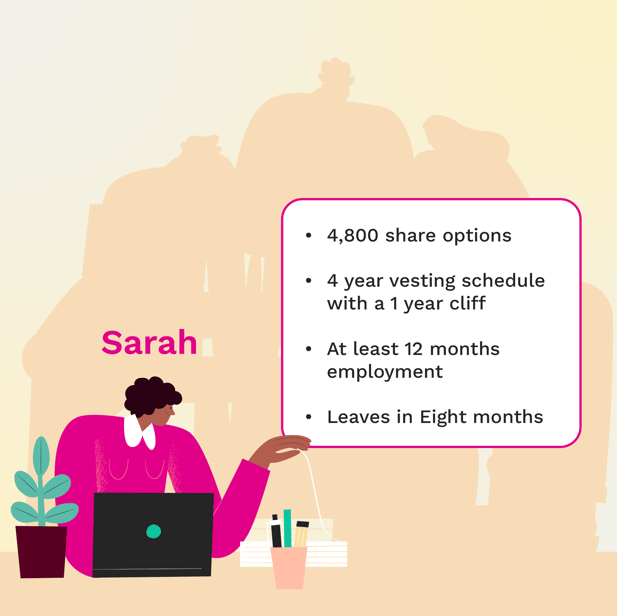

Understanding vesting is much easier when you see it in action. Here are four common situations employees and founders encounter.

Outcome: Sarah receives no equity and forfeits her entire option grant.

This is exactly why cliffs exist. They help companies avoid issuing ownership to employees who leave shortly after joining, while ensuring equity is reserved for those who make a longer-term contribution.

Key takeaway: If an employee leaves before the cliff date, they will usually lose their entire option grant.

.png?width=617&height=617&name=2%20(1).png)

Outcome:

In most employee share schemes, Tom keeps the options he has already earned, subject to the scheme's exercise rules and deadlines. However, the remaining unvested options are typically cancelled and returned to the company's option pool.

Key takeaway: Employees generally keep what they have earned through vesting but lose any options that have not yet vested.

.png?width=2084&height=2084&name=3%20(2).png)

Outcome: The same acquisition can produce very different outcomes depending on how the plan is structured.

Key takeaway: Acquisitions do not automatically accelerate vesting. Employees should always check the acceleration provisions in their option agreement.

.png?width=2084&height=2084&name=4%20(1).png)

Outcome: Employees can accumulate several overlapping option grants throughout their careers.

Key takeaway: Promotions often lead to additional option grants, creating multiple vesting schedules that need to be managed and tracked separately.

The answer depends on the circumstances.

Employees should always review the specific rules governing their share scheme.

Even experienced employees can misunderstand how equity works.

Many of these challenges stem from manual processes and limited visibility. Discover how Vestd makes managing vesting schedules, grants, and ownership records significantly easier.

The difference between granting equity and creating ownership often comes down to vesting. Get it right, and employees gain a clearer connection to the value they're helping create.

Ready to take the complexity out of vesting? Book a personalised demo and see how Vestd makes employee ownership easier to manage at every stage of growth.

Imagine you're one of the first employees at a fast-growing startup. Along with your salary, you're offered 20,000 ESOPs. It sounds exciting, but...

A common misconception about ESOPs is that once you've been granted stock options, they're yours no matter what happens. In reality, what you walk...

Employee Stock Ownership Plans (ESOPs) have become one of the most popular ways for startups and private companies to attract, reward and retain...