If your employer has issued you EMI options, you’re the beneficiary of a tax-advantageous share scheme. You can read more about the tax benefits of EMI, but here we’ll explain how your EMI options are issued over a growth share class and what that means for you.

Usually, EMI options are issued over an ordinary share class. This means that when you decide to exercise your options, you’ll have to pay the agreed exercise price set by the company (this is usually the actual market value (AMV) of the shares at the time of issue).

If you work for an established company or have thousands of options to exercise, the cost to exercise your options and own the shares can be expensive. For example, say your company issues you 1,000 options with an exercise price of £5 per share, you’d have to pay £5,000 to own the shares.

Of course, the shares might be worth a lot more than £5 when you exercise your options, but not everyone has the funds to cover the initial exercise price.

However, when a company issues EMI options over a growth share class, the exercise price becomes significantly lower as growth shares are always issued at nominal value (the face value of a share, as determined by how the company’s capital is denominated) or close to. This can be anything from £1 - £0.00001.

Growth shares are essentially worthless upon issue as they have a ‘hurdle rate’ attached to them, which is the value in which the recipient starts to benefit from the shares.

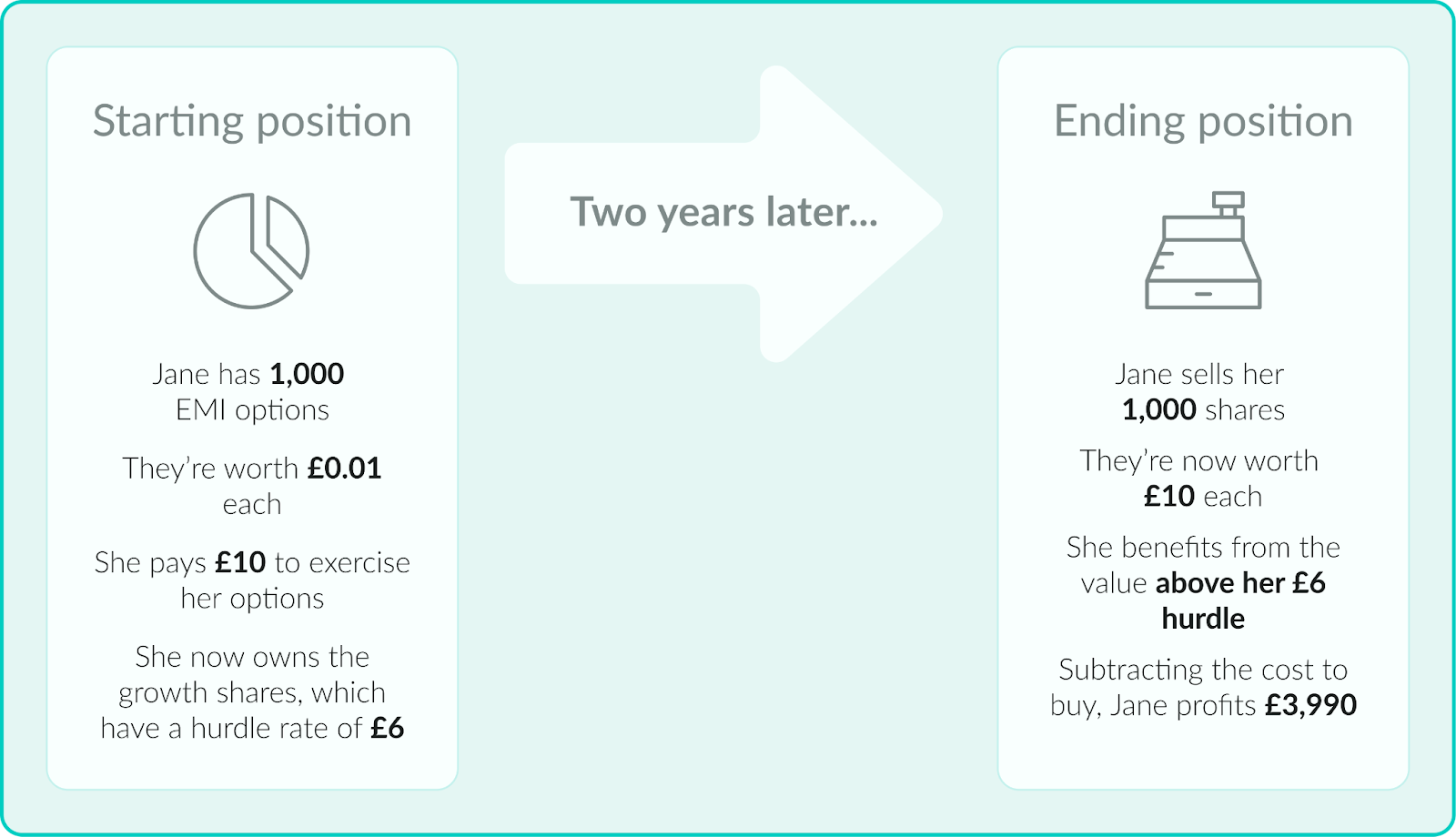

For example, Jane has received 1,000 EMI options that use a growth share class. At the time, the company is valued at £5 per share, but Jane’s growth shares are issued at £0.01 with a hurdle rate of £6.

Exercising these options is a fraction of the cost compared to ordinary shares, but the first £6 of the shares is reserved for ordinary shareholders.

So when Jane eventually sells her shares, she will benefit from the share price at the time of sale minus the hurdle rate.

Why do companies set hurdles?

Hurdles protect existing shareholders from dilution when new shares are issued. They also ensure new shareholders don’t benefit from the work of the people before them.

Continuing from the example above, if a new employee had the same hurdle of £6 when the shares are now worth £10, it wouldn’t be fair to you if they profit from the work you’ve done to grow the company to £10 per share. Instead, their hurdle will be higher to reflect the value they add to the company from that point onwards.

Our team, content and app can help you make informed decisions. However, any guidance and support should not be considered as 'legal, tax or financial advice.'