TLDR: When a recipient is ready to exercise their options, they submit a request through Vestd. The company's admin user then reviews and processes it, confirming the company valuation and any relevant tax or legal considerations. Once processed, the recipient is notified and issued a share certificate. Payments are handled outside of Vestd.

So, you've made the incredible decision to implement a share option scheme to incentivize your employees and those committed to delivering exceptional results for your company. That's fantastic! 🎊

Now that they've achieved their goals or adhered to the terms of their option agreements, it's time for them to exercise their options.

But how does this process actually work? 🤔

Let's walk through how share scheme recipients can exercise their options on the Vestd platform, and how admin users can ensure everything runs smoothly.

Contents📋

- For recipients: How to request to exercise your options

- For admin users: Processing exercise requests

- Back to recipients: What happens next

- Final steps for admin users: Issuing the share certificate

- Need support?

For recipients: How to request to exercise your options 🎯

Log into your Vestd account and you’ll arrive at your My Equity page.

Here, you'll find all your option grants neatly displayed in rectangular boxes 📦. Each box represents a different option grant, so if you have multiple grants, you'll see multiple boxes.

In each box, you'll see important details like the type of option grant (e.g., EMI), and the number of options that are vested, unvested, and exercised. For instance, you might see that you have 250 options vested but none exercised yet.

Ready to exercise some of your options? Here's how you can do it:

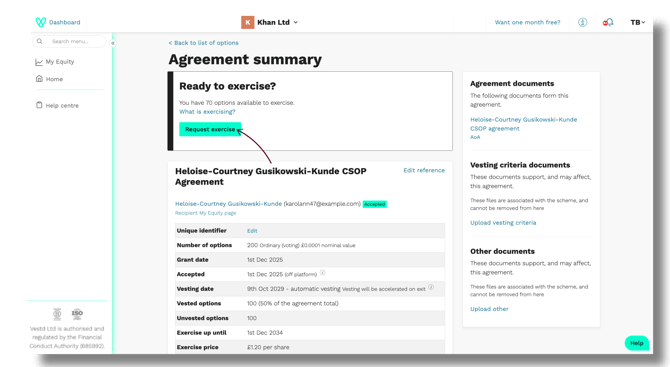

- Access Your Option Agreement Summary: Click on the View Agreement Summary button on the right-hand side of the option grant box. This will take you to the summary page for that specific option grant.

2. Initiate the exercise request

At the top of the summary page, you'll see a "Ready to exercise?" box. It shows how many eligible options you have, plus a link to this our guide on What is exercising? When you're ready, click Request exercise to get started.

3. Specify the number of options: You'll be directed to a page where you can enter how many of your vested options you'd like to exercise. Here, you'll also find information about any potential tax liabilities based on the exercise price and the Actual Market Value (AMV) of the shares at the time of grant.

- Enter the number of options you’d like to exercise in the field provided under Number of Ordinary options to exercise.

- Tick the checkbox acknowledging that you'll need to pay the company separately for the exercise of your options.

- Once everything looks good, click Submit Request.

🚨 Important: Payments are managed outside of Vestd. Both the recipient and the company are fully responsible for tracking and managing these transactions.

After submitting, you'll be redirected back to your Option Agreement Summary page. A banner at the top will confirm that your exercise request has been sent to the company.

For admin users: Processing exercise requests 🛠️

As an admin user responsible for managing tasks on the Vestd platform, you'll receive an email notification when a recipient submits an exercise request. This email will inform you of the number of options they're looking to exercise and the total purchase/exercise price.

Here's what you need to do:

- Click the green View Exercise Request button in the email to review the exercise request

-

- HMRC Reporting: Remember that the exercise event must be reported in your annual notification to HMRC. You can find more details in our How to file your annual return through HMRC's ERS system Guide.

- EMI Tax Benefits: There are tax benefits associated with EMI options. Learn more in our EMI Tax Benefits Guide.

- ITEPA S431 Election: Determine whether a Section 431 election needs to be signed. This election can affect the tax treatment of the shares. Our ITEPA S431 Guide can help you decide.

- Deed of Adherence: Check if a deed of adherence to any existing shareholder agreements needs to be signed. More information is available in our Deed of Adherence Guide.

-

- Yes, the most recent valuation is correct. If you choose this, you'll proceed with the current valuation.

- No, a new valuation is needed. If material changes have occurred since the last valuation, you'll need to update it. Clicking this option will allow you to either request a new valuation from Vestd or record an existing valuation. Not sure what counts as a material change? Click the hyperlinked ‘What constitutes a material change’ dropdown.

- No, continue exercise without a valuation. Proceeding without a current valuation is not recommended, as it can affect your HMRC reporting and corporation tax relief claims.

For this example, let's assume you select Yes, the most recent valuation is correct

🚨 Important: Payments are managed outside of Vestd. Both the recipient and the company are fully responsible for tracking and managing these transactions.

4. Process the Exercise Request: After confirming the valuation is correct, and reviewing the exercise price and total payment amount, click Process exercise request.

A pop-up will inform you that the platform will generate and submit an SH01 form to Companies House to record the share issuance resulting from the exercise. The recipient will then be added as a shareholder to the cap table.

5. Finalise the Process: Confirm that you're ready to proceed. Once you click Continue, the exercise request will be completed. A banner notification will appear, letting you know that the recipient has been notified.

Back to recipients: what happens next

After the admin user processes your request, you'll receive an email confirming that the requested number of shares (options) have been exercised. The notification will also mention any tax liabilities you need to be aware of.

- Click the green View option button in the email.

2. This will take you back to your Option Agreement Summary page.

3. Check Your Exercise History: You'll notice that the number of options you've exercised is now reflected in your summary.

4. Scrolling down, you can see your Exercise history, which provides details of all your exercises.

5. See the changes on your My Equity page: Returning to your My Equity page, you'll see the progress bar in your option grant box has updated to show that a portion of your options have been exercised.

Final steps for admin users: Issuing the share certificate 📜

With the exercise request completed, the next step is to issue the share certificate to the recipient.

- Receive Notification: You'll get an email informing you that the share certificate for the recipient is ready for signing. Click "View and send for signing".

-

- You'll be taken to the Share Certificates page.

- If you need to update the signatories (those who need to sign the certificate), click Update settings and make the necessary changes. Our Share Certificate Settings’ guide can assist you.

- Locate the recipient's share certificate at the top of the list. You'll see details like the recipient's name, the number of shares, and the share class.

- The status will show as Draft.

- Preview the certificate by clicking the eye icon. Ensure all details are correct.

- When you're ready the share certificate for signing, click the envelope icon

5. Monitor the Signing Process:

- Back on the Share certificates page, you can see the status of the certificate.

- Once all required parties have signed, the status will change to a green tick. The recipient will then receive their signed share certificate.

![]()

And There You Have It! 🎉

That's the complete process for exercising options on the Vestd platform, both from the recipient's perspective and the admin user's. By following these steps, recipients can smoothly exercise their options, and admin users can efficiently facilitate and complete the process.

Need support?

If you have any questions, our dedicated Customer Success team is here to help: support@vestd.com

Not onboard yet? Hop on a call.

Our team, content and app can help you make informed decisions. However, any guidance and support should not be considered as 'legal, tax or financial advice.'